3 / 5

3 / 5

ON FRIDAY

SEPTEMBER 18, 2015

SabahandSarawak

property

outlook

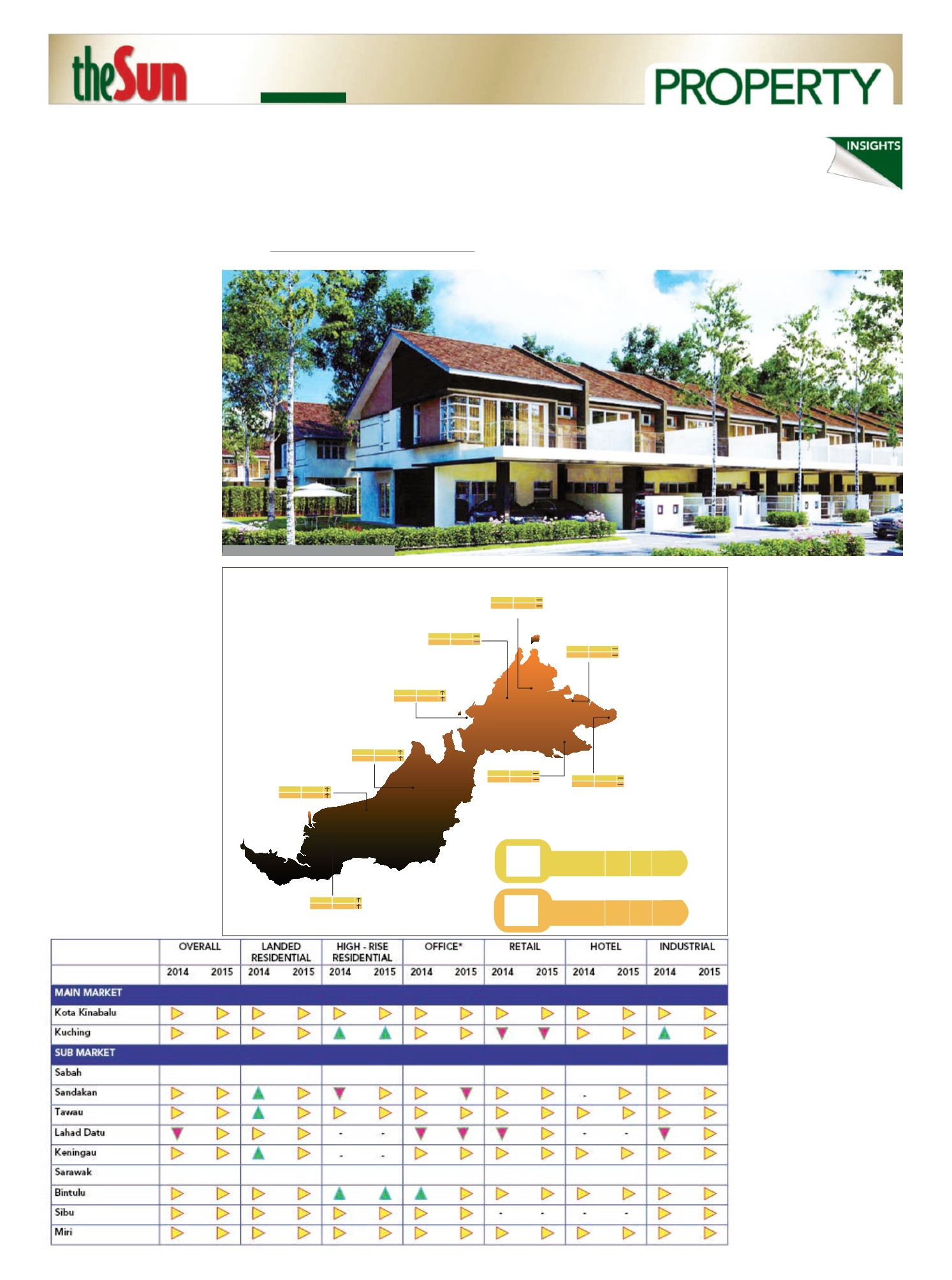

> Propertymarket overview

KotaKinabalu

Sandakan

Lahad Datu

Tawau

Sibu

Bintulu

Miri

Labuan

Keningau

>

<

>

<

>

<

>

<

>

<

>

<

>

<

>

<

>

<

>

<

600,000 650,000

1,000,000

1,100,000

400,000

420,000

700,000

750,000

360,000

420,000

550,000

620,000

301,000

322,000

432,000

552,000

327,000

370,000

522,000

581,000

342,000

495,000

392,000

599,000

366,000

573,000

482,000

648,000

396,000

587,000

220,000

380,000

500,000

250,000

422,000

577,000

Legend:

AverageTransacted Price of 2

storeyTerraced House

(RM per unit)

Year

2013

Year

2014

2015

Outlook

Average Transacted Price of 2

storey Semi-Detached House

(RM per unit)

Year

2013

Year

2014

2015

Outlook

TURN TO

PAGE 26

X

W

HILE

a report citing

Institut Rakyat director

Yin Shao Loong

mentioned that Sabah

has themost expensive homes in

Malaysia, costing some 11 times

more than a family’s median annual

income of RM34,320 (followed by

Sarawak, then Kuala Lumpur), a

study by CHWilliams TalharWong

and Yeo on the property scene in

Sarawak signalled growth in the last

five years.

SARAWAK SCENE

CHWilliams TalharWong &Yeo

managing director Robert Ting

states: “There has been a hike in

property prices in Sarawak over the

last five years, recording impressive

increases of between 10% and 15%

per annumor evenmore, especially

for prime residential and

commercial units. The residential

sector has seen a shift, to high-rise

residential developments especially

in the urban areas of themajor

towns and cities such as Kuching,

where high-rise residential

developments have even exceeded

that of landed residential for its

urban area. There has also been a

huge growth in the commercial

sector for Sarawak with high

numbers of shophouse units coming

into themarket in the last few years,

as well as the proliferation of retail

space which has increased bymore

than twomillion sq ft for Kuching in

the past five years and close to four

million sq ft in the last eight years.”

Ting adds that although the

market has been growing at a

prolific rate in the last five years, it

seems to be slowing down in terms

of take-up rates. However, prices

are still increasing albeit at a lower

rate. Price adjustments have also

begun due to the implementation of

GST.

In all, Ting feels that the

propertymarket in Sarawak will

continue to be positive. However,

property developers will see a

slower intake of properties – “a

decline in volume of sales. In short –

prices will increase but transactions

will slowdown”.

In fact, some sectors are already

showing signs of saturation such as

the commercial shophouse and

retail sector with increasing

vacancy rates and negotiable and

reduced rentals. Themarket seems

to have “softened” and sales are

somewhat dampened by the low

buyers’ sentiment following the

latest negative developments in the

economic and political arena of the

country.

Prices of property in Sarawak is

fairly low comparedwith KL. Then

again, Ting adds, the rate of

increase has been “scary” in recent

years. “This is due to the generally

lower average household income in

Sarawak comparedwith KL. There

will be increasing disparity between

what themarket is offering and the

demand of the general population

should property price continue to

increase at the rate it has been rising

at. Affordability of property in

Sarawak is now an issue and a

pressing problem to provide good

basic housing for the community at

large,” Ting commented.

SABAH STANDING

Over in Sabah, CHWilliams Talhar

&Wong (Sabah) managing director

Robin Chung shared his views. “For

Sabah, in general, the property

market has been quite active with a

number of newdevelopments

launched (especially in Kota

Kinabalu), which has also been

going through a growth phase in the

earlier part of the last five years

with a rise in property prices. But

the decline in commodity prices (i.

e. CPO-profits fromoil palmbeing

one of themain drivers of the

propertymarket) in the later part of

2012, the Central Bank’s

implementation of tighter lending

guidelines and coolingmeasures

between 2012 and 2014, plus buyers’

difficulty in getting loans approved

as well as less favourable economic

conditions of late … these have seen

more cautious sentiments and

transaction activities taking a

breather with prices levelling off.”

Price wise compared to KL

property, Chung reveals that the

newor on-going condominiums in

KKCBD ranges between RM700

and RM1,000 per sq ft … “roughly

averaging to RM800 to RM850 per

Taman Rimba, Phase 3, KotaKinabalu.