5 / 5

5 / 5

C

ONTINUING

from last

week’s article on the

sub-sale market in which

we defined the term and

disclosed the local scene and

statistics, this week we highlight

dos and don’ts in purchasing a sub-

sale residential property in

Malaysia.

POINTS TO CONSIDER

According to personal finance

guide KC Lau, there are a few

important matters one needs to

consider when intending to

purchase a sub-sale or

“secondhand” residential

property. Other than the location,

which is numero uno, one needs

to deliberate on these other

important issues:

Property type i.e. landed

property or high-rise/serviced

The size

Number of bedrooms

Facilities

The age and “lifespan” of the

property

The tenure

Purpose of purchase i.e.

investment to rent or re-sell, or

stay

Amenities and conveniences

Safety features

Market value

Selling price

Once all the above are

contemplated and decided on, the

next thing to do is check the sub-

sale listings, one of which

we recommend being

iproperty.com.my,under the REA

Group, recently

tying up with

India’s Elara

Technologies.

The online

property site gives

access to 4.5 million

property listings across

72 countries via various

portals.

In the meantime, while

hunting for that perfect

place to call home or

to invest in, it is best

to check with the

banks if you plan on

taking up a loan. Do

research to find the best

home loans.

Websites like

iproperty.com.mymakes life easier by

providing a “loan

X

X

X

X

X

X

X

X

X

X

X

calculator”. You could also check

with individual banks on loan

packages and offers, and get the

bank to do a valuation and

assessment on the property you

intend to buy. It is advised that

you get three “independent” banks

to do the valuation.

PLANAND BUDGET

Next step is to plan your budget,

irrespective of buying cash or

taking a bank loan. This is due to

the various fees and charges

incurredwhen buying sub-sale

property.

According to Lau, the

proportion or percentage of down

payment is crucial. This will give

the buyer a sense of howmuch

cash he needs to put upfront.

Other payments that need to be

considered include:

> Residential buy checklists, tips and advice

Sub-sale propertymarket

PART2

List of documents required for standard bank loan application

Copy of IC

3 months’ payslips (fixed salary)

3 months’ bank statement showing crediting of salary

Previous year’s income tax returnwith payment receipt

Latest EPF statement

Liquidity backup i.e. fixed deposit, saving/current account

Other source of income such as rental income substantiated by

stamped tenancy agreement and bank statement

Booking form

Application form

X

X

X

X

X

X

X

X

X

List of disbursements and legal fees involved

Legal Fees

Sale and Purchase Agreement

Entry&withdrawal of private caveat

Submission of Borang CKHT 2A

6%government tax.

Disbursements

Stamp duty on the Sale and Purchase Agreement

Stamp duty on the transfer

Title search

Registration fee on the transfer

Registration fee on the entry andwithdrawal of private caveat

Bankruptcy/winding up search

Affirmation fee on surat akuan

Transport charges

Telephone charges

X

X

X

X

X

X

X

X

X

X

X

X

X

Email your feedback and

queries to: propertyqs@

thesundaily.comX

Legal fees

Property stamp duty charges

Loan agreement stamp duty

Disbursement fees which cover

registration of charge, land

search and bankruptcy search

Loan processing fee

An earnest deposit is usually

requiredwhen one has already

decided to buy a particular sub-

sale property. The amount is

usually 1% to 2%of the agreed

property price. Once this sum is

paid, a deal ismade and buyer and

seller are bound.

As the purchaser, youwill need

to appoint a lawyer to act on your

behalf.

In themeantime, your bank

loan/mortgage planwill need to

be settled. This covers loan type,

amount, description of property,

duration of loan, fees,

monthly service

charge, interest and

repayment,

instalments, security

and insurance

documents, excess

interest rates,

Mortgage Reducing

TermAssurance

(MRTA) or Group

Mortgage Term

Assurance

(GMTA) if any,

and other conditions.

HOUSE

CONTENTS

AND

CONDITION

Amajor area

many overlook

when buying sub-

sale property is

the recce, also

known as the “fact

finding visit”

X

X

X

X

X

according to

Lau. One

needs to draw

up an

inventory list,

stating items

the seller will

leave within

the property

and those he/

she will

remove. Best

state the

condition the

said “items”

are in.

The

signing of the

“Sales and Purchase Agreement”,

otherwise known as the SPA, is

next, along with settlement of any

outstanding payments, and the

solicitor’s bill. As the buyer, it is

good to ensure that the condition

of the premises and its contents

are correctly described in the

SPA.

A valuation report will be

conducted by the bank of which

youwill need to bear the report

charges. A home loan account will

be set up along with the bank loan

agreement.

If buying a high-rise sub-sale

unit i.e. condominiumunit, there

should be amaster insurance

policymaintained by the company

in charge of managing the

building, of which the charges are

usually incurred in your monthly

condominiummaintenance fee.

Partial and full disbursements

will need to be settled by this time.

This is when the seller will need

to settle all outstanding loans/

amounts with his/her bank on the

property and you, the buyer, will

need tomake all necessary

payments between your bank and

the seller’s bank.

This is also a crucial period

when the seller will need to

deliver “vacant possession” of the

sold premises within a specified

timeframe according to the SPA.

For a detailed step-by-step

guide, samples of forms and

checklists, visit the KCLau.com

website. For a comprehensive

listing of sub-sale properties, visit

iproperty.com.myFollowour property section next

week for additional information

on the sub-salemarket.

[Lists , information and charts

retrieved fromKC Lau and

iProperty.com]

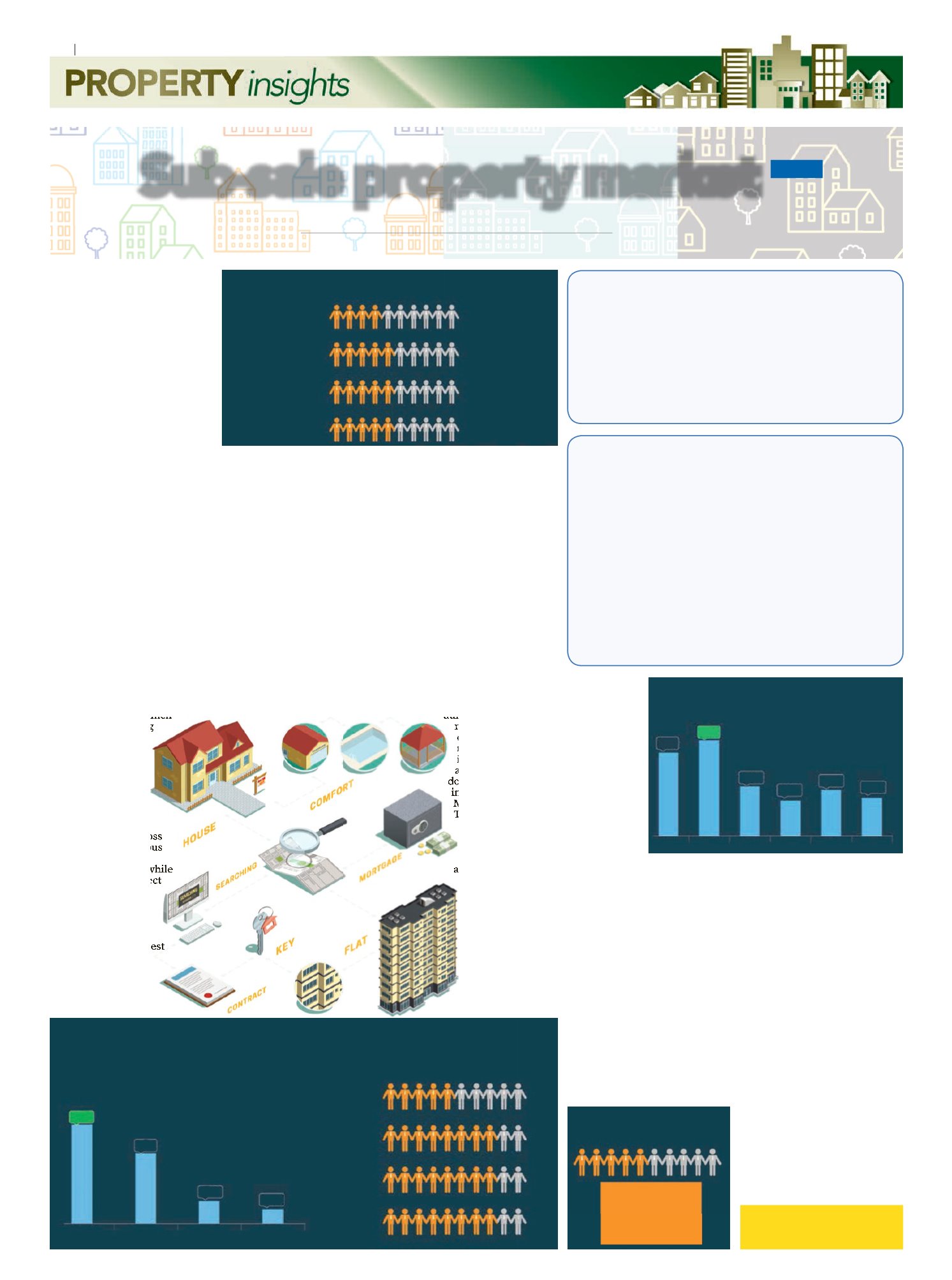

PURCHASED PROPERTY BELOW 1,000 SQ FT – TOP STATES

Kuala Lumpur

40%

Selangor

50%

Johor

50%

50%

Penang

WHAT BUYERS PAID FOR A

RESIDENTIAL PROPERTY IN MALAYSIA

48%

34%

11%

7%

Below250k 250-500k

500-850k Above850k

BELOW RM500K MARKET SHARE

IN TOP STATES

Kuala

Lumpur

50%

80%

80%

80%

Selangor

Johor

Penang

DOES SIZE MATTER?

50

%

Bought a property below

1,000

sq ft

SIZE MARKET SHARE – MALAYSIA

24

%

28

%

14

%

10

%

13

%

11

%

501-750 sq ft

751-1,000 sq ft

1,001-1,250 sq ft

1,250-1,500 sq ft

1,501-2,000 sq ft

Above 2,000 sq ft

20

theSun ON FRIDAY

|

MARCH 11, 2016

22

theSun ON FRIDAY

|

JUNE 23, 2017