2 / 5

2 / 5

20

theSun ON FRIDAY

|

MARCH 11, 2016

24

theSun ON FRIDAY

|

MARCH 10, 2017

>Comments and observations of key players

at iProperty.comMalaysia and Brickz.my

Views

on

property

coolingmeasures

V

ARIOUS

coolingmeasures

introduced by the

Malaysian government and

Bank NegaraMalaysia

(BNM) to help curb escalating

property prices has had little

impact, said iProperty.com

Malaysia and Singapore CEO

Haresh Khoobchandani. Together

with Brickz.com, the company

analysed data fromBNMand the

Valuation and Property Services

Department of Malaysia (JPPH) to

examine if the measures introduced

over the years actually impacted the

residential and financial markets.

theSun

reports the study conducted.

“From the data we got, we saw

that prices for residential property

inMalaysia had been sky-rocketing

since year 2000. Between 2008 and

Q2 of 2009, following the sub-prime

mortgage crisis in the US, which

affected economies around the

world, house prices experienced

nearly no growth. The number of

loans approved for residential

properties also decreased the same

year as themarket moved funds

away from the softening real estate

market,” Haresh said.

Based on figures in theMalaysia

Residential Loans andNational

House Price Index (HPI), it was

learned that the annual quarter-on-

quarter national HPI began to

increase the highest from 2011-Q1 to

2012-Q1.

In 2011-Q1, the HPI was at 149.1,

while in 2012-Q1, the HPI was at 167.

Thus, the difference shows an

increase of 17.9 index points in 2011.

For the same period, performance

for residential loans approvedwas

stable at RM20.4 billion. The data

showed that the quarter-on-quarter

HPI had slowed down to a growth

of 15.3 index points between 2015-Q1

and 2016-Q1. Performance for

approved residential loans also fell

2007

It was reported that in 2007, the

Developer Interest Bearing

Scheme (DIBS) was first introduced

by a property developer in

Penang, as a precursor to the

Built-Then-Sell (BTS) 10-90

concept stated in the Housing

Development (Control and

Licensing) Regulations, 1989

(amended 2007). At that time, the

demand in the real estate market

was high and property developers

were offering creative products

andmarketing schemes to attract

house buyers. It can be observed

that the total housing loans

approved went up by 59.57%

(RM5.07 billion) for quarter-on-

quarter change in 2008 Q1

2008 TO 2009 Q2

House prices in Malaysia only had

a growth of 0.9 index points in

2009 (Table 1) during the sub-

prime mortgage crisis in the US

which also affected economies

around the world. It can also be

observed that the amount of loans

approved for residential properties

suffered a contraction. In the same

year the total housing loans

approved fell by 14.13% (RM1.91

billion).

TIMELINE

Email your feedback and

queries to: propertyqs@

thesundaily.comX

drastically by RM5.6 billion from

2015-Q1 to 2016-Q1. HPI however,

continued to rise despite a drop in

the amount of residential loans

approved since 2014.

“In our opinion, the drop in loans

approvedwas contributed by all the

previous interventions introduced

by BankNegara and the

government. The interventions

did not reduce the property prices

but did slowdown the growth,”

Haresh said.

Brickz.my founder Premendran

Pathmanathan, who is also

iProperty.comMalaysia’s data

services general manager said that

themeasures introduced by the

government, including removal of

the Developer Interest Bearing

Scheme (DIBS), had actually

decelerated demand.

“Other factors that could also put

tha brakes on demand could be due

to the changes in real property gains

tax (RPGT), revision in loan to

value (LTV) curbs and also the

introduction of the Goods &

Services Tax (GST). Aside from

this, the global uncertainty,

weakening ringgit, and change in

price (drop) of oil and gas has also

played a role in this as well,”

Premendran reasoned.

“The DIBS scheme only required

an initial payment of 5%or 10%of

the property price. So, purchasing

property became an attractive

option for investors. It was likely

that the increase in the price of new

properties from 2011, were the result

of speculative buying due to the

scheme,” Premendran said.

Haresh however, felt that the

coolingmeasures had actually

impacted the financial sector and

also reduced negative sentiments of

the oversupplied housingmarket.

“If you look at the data, the price

index for houses continued to climb

at double digit rates, by 15.3 index

points in Q1 2016, while the financial

sector on housing loans fell 23.24%.

The various measures introduced

appeared to have consolidated the

financial sector and reduced the

negative sentiments of the

oversupplied housingmarket,”

he said.

“It is unlikely that prices will

decrease, instead likely to stabilise

or increase at a slower rate in

coming years. This is primarily due

to the fact that we have a growing

young adult population and this is

driving the demand for property,

which in turnwill continue to place

upward pressure on prices.

“With the real estate industry

now consolidating, the industry

may shift their focus toward

developments that apply to

affordable living. Infrastructure

such as transportation, energy and

social infrastructure will help to

increase economic efficiency and

reduce the cost of living, thus

making locations that once

seemed expensive to live in now

more affordable.”

In all, Haresh believes the above

is why property buyers and

investors are adopting a cautious

approach and are being very

selective inwhere andwhat they

choose to purchase. “There is

increased demand for affordable

homes, particularly through a

growing, young population looking

for properties in the major urban

centres. “WhileMalaysians are

concerned about the rising house

prices and affordability, property is

still viewed the most attractive

investment choice and this is due to

capital growth opportunities. It is

alsomore stable compared to other

assets,” he said.

[Information and images from

iProperty.com]

2010

InNovember 2010, BankNegara

Malaysia (BNM) implemented the

policy of amaximum loan-to-value

(LTV) ratio of 70%, whichwill be

applicable to the third house

financing facility by a borrower. The

policy aimed at moderating the

excessive investment and speculative

activity in the residential property

market.

2011

It is strongly believed that the

increase in the prices of newly

launchedproperties (primarymarket)

beginning in 2011 are the results of

speculative buying. At that timeDIBS

was popular amongproperty

developers to attract ordinary house

buyers. The scheme alsomade it

cheap for speculators to earn

relatively large profits because it only

warrants an initial 5%or 10%of

property price and two to three

years’ time period for them to sell the

investments. FromApril to July 2011,

BNMhas raised the Statutory

Reserve Requirement (SRR) Ratio

three times to 4% from1%. It is

observed that therewas a large shift

in global liquidity which resulted in

significant capital flows into

emerging economies, particularly

theAsian region. The decision to

raise the SRRwas undertaken as a

pre-emptivemeasure tomanage the

risk of this build-up of liquidity. From

Table 1, annual quarter-on-quarter

national House Price Index (HPI)

began to increase the highest from

2011-Q1 to 2012-Q1. In 2011-Q1, HPI

was at 149.1, while in 2012-Q1HPI

was at 167. Thus, the difference

shows an increase of 17.9 index

points in 2011. For the same period,

performance for residential loans

approved ismaintained at RM20.4

billion.

2012

In January 2012, BNM issued

guidelines requiring financial

institutions tomake appropriate

enquiries into a prospective

borrower’s income after statutory

deductions for tax and EPF, and

consider all debt obligations in

assessing affordability. The

guidelines promote better

protection for financial consumers

and a sustainable credit market. The

government has also revised the Real

PropertyGains Tax (RPGT) to 10%

from5% for properties held and

disposedwithin two years as the

previous rate of 5% is not effective in

curbing real estate speculative

activities. The government have also

expandedMy First Home Scheme to

help those earningbelowRM3,000

by increasing the limit of house prices

qualified to RM400k fromRM200k.

The scheme is available to house

buyers through joint loans of

husband and wife. At the same time,

the high sovereign debt within the

Eurozone was posing a threat to

global economies. It started in 2009

whenGreece was at risk of

defaulting its debt. There were

allayed fears that Malaysia’s current

government debt toGross Domestic

Product (GDP) ratio of 53.3% in 2012

was vulnerable to any economic

collapse from the Eurozone.

Malaysia’s government debt toGDP

ratio has always hovered below the

limit of 55% since 2010. Meanwhile,

the country’s gross external debt

which includes external offshore,

public enterprises and private

sectors loans) toGDP ratio has been

rising from62% (RM602 billion) to

72.1% (RM833 billion) from2012 to

2015.

2013

Loans approved for residential

properties climbed in 2013. In

November, BNM issued guidelines

to banks tightening lending

practices which include abolishment

of Developer Interest Bearing

Scheme (DIBS) and enforcement of

stricter LTV ratio calculations, while

the government imposed a higher

RPGT at 15% for properties held and

disposed within 2 years and 10% for

properties held and disposed

between two to five years.

2014

It can be observed that following

the counter measures taken in 2014

such as revision of RPGT and curbs

on LTV ratio, the amount of loans

approved the following year in 2015

fell by 4.38% (RM1.11 billion) while

Q1 quarter-on-quarter change in

HPI for 2015 increased by 15.8 index

points (Table 1).

2015

In June 2015, theNational Higher

Education Fund Corporation

(PTPTN) began listing borrowers

who have never paid back their

loans into Central Credit Reference

Information System (CCRIS). It has

been reported that 30%of the loans

submitted in 2016 were rejected

due to applicant’s debts with

PTPTN. FromTable 1, quarter-on-

quarter HPI has slowed to a growth

of 15.3 index points between 2015-

Q1 to 2016-Q1. Recall earlier on that

in 2011, HPI increased by 17.9 index

points. Performance for residential

loans approved also fell drastically

by RM5.6 billion from2015-Q1 to

2016-Q1. HPI continues to rise

(moving towards right) despite a

drop in the amount of residential

loans approved since 2014.

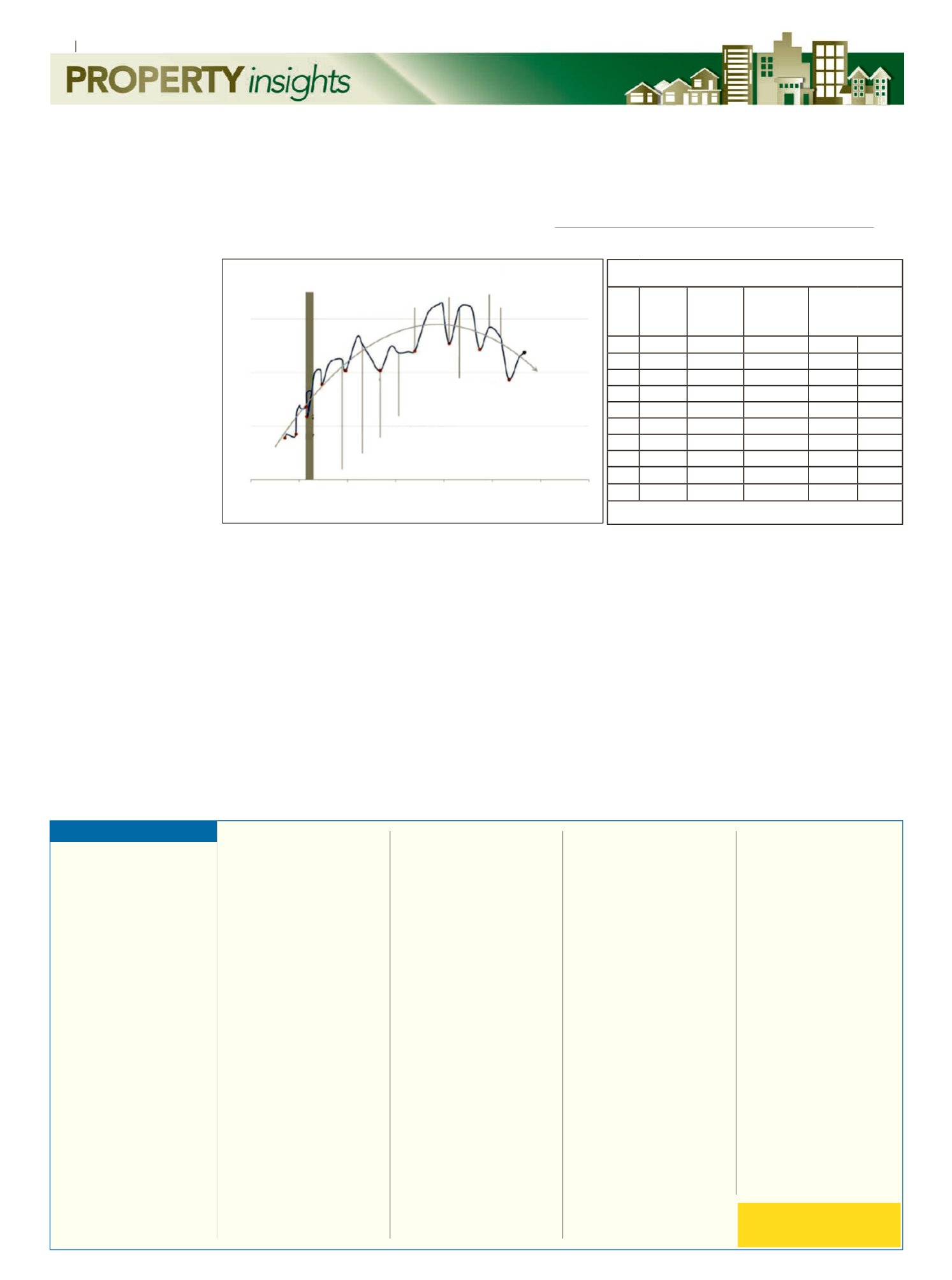

Chart 1: Relationshipbetween loanapprovals andNational HousePrice Index (HPI)

U.S.sub-primemortgagecrisis

RPGTrevisionand

abolishmentofDIBS

RPGTrevisionandLVTratio

curbs

GSTimplementation

PTPTNblacklisting

HPI=241.6

RM23.8bil

Q3

2016

2015

2014

2013

2012

2011

2010

2009

2007

2006

2008

MYR1millionlimitpolicy

forforeignbuyers

Eurozonesovereign

debtcrisispeaked

RPGTrevisionandhigherscrutiny

intoborrower’sincome

SRRraised3timesfrom1%to4%

70%LVTratiofor3rdhouse

financing

HouseLoansApproved (inRMbillion)

30

20

10

0

100

125

150

175 200 225

250

275

NationalHousePriceIndex(Year2000=100)

Source:BankNegaraMalaysiaandValuationandPropertyServicesDepartmentofMalaysia

Table1:NationalHPIandHousingLoansApprovedforQ1and

Year-On-YearChange

Period National

House

PriceIndex

forQ1

Change

National

HousePrice

IndexforQ1

HousingLoans

Approvedfor

Q1(MYR‘000)

Change inHousing

LoansApprovedfor

Q1(MYR‘000and

percentage)

2007 123.4

+5.7

8,

516,435 694,703 8.88%

2008 128.7

+5.3

13,589,771 5,073,336 59.57%

2009 129.6

+0.9

11,669,915

-1,919,856 -14.13%

2010 136.9

+7.3

17,788,834 6,118,919 52.43%

2011 149.1

+12.2

20,363,494 2,574,660 14.47%

2012 167.0

+17.9

20,371,468

7,974

0.04%

2013 184.9

+17.9

23,985,479 3,614,011 17.74%

2014 202.7

+17.8

25,418,331 1,432,852 5.97%

2015 218.5

+15.8

24,305,339

-1,112,992

-

4.38%

2016 233.8

+15.3

18,657,200

-

5,648,139 -23.24%

Source:BankNegaraMalaysiaandValuationandPropertyServicesDepartmentof

Malaysia