4 / 4

4 / 4

Email your feedback and

queries to: propertyqs@

thesundaily.comX

H

AVING

covered both the

sub-sale residential

markets in Sabah and

Sarawak over the last two

weeks, we highlight the outlook in

Selangor via this brief summary by

iProperty Group data services

general manager Premendran

Pathmanathan.

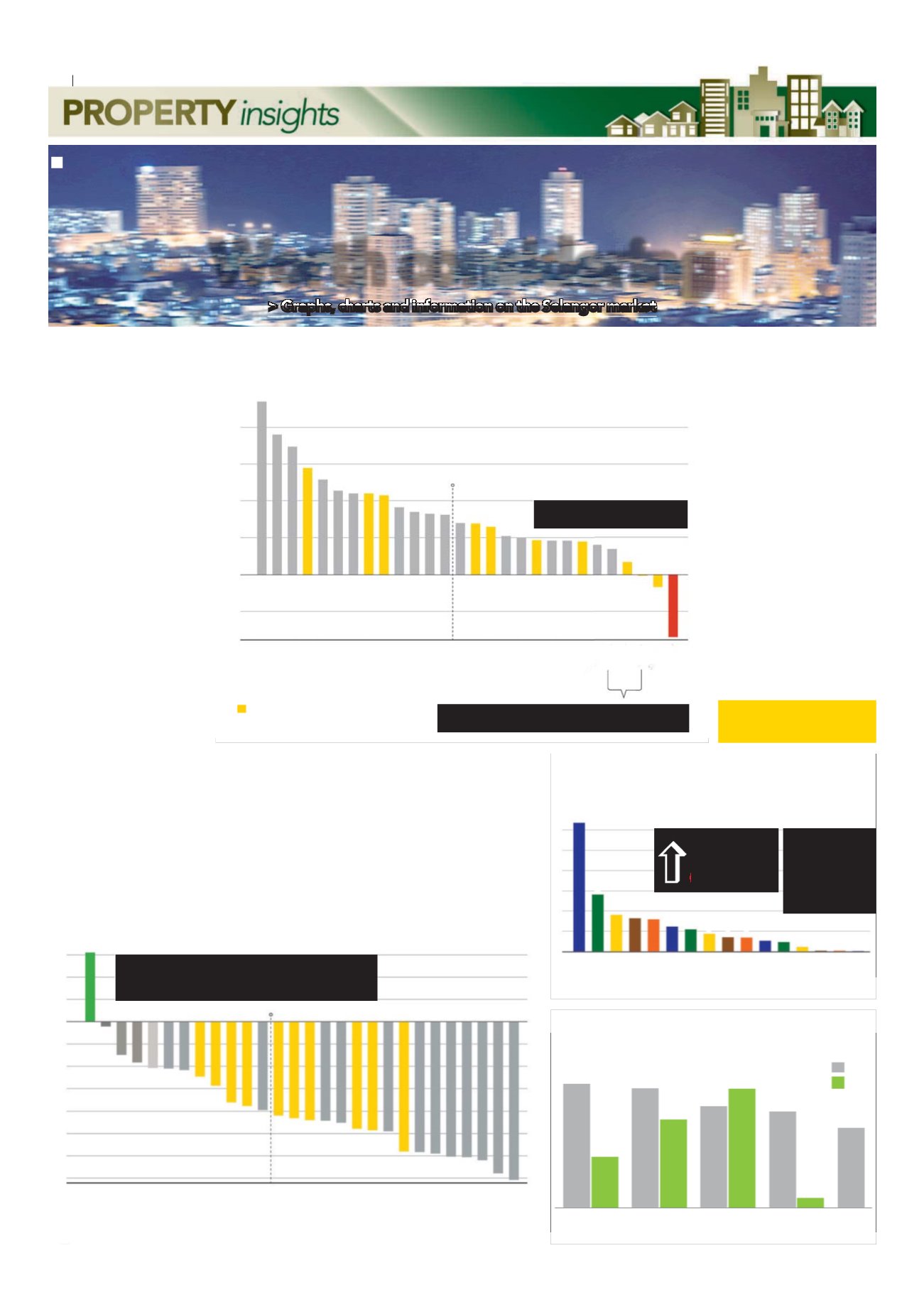

In terms of sales volume,

Selangor emerged the best-

performing state against the

country’s market share (refer C).

Although there was a drop of 17.6%,

looking at year-on-year (Y-O-Y)

figures, Selangor achieved 31.7%

(28,467 transactions) according to

data retrieved betweenNovember

2015 andOctober 2016.

Interestingly, Penang was the

only state which performed better

thanMalaysia’s average (-20.4%),

while Kelantanwas the only state

that recorded a positive trendwhere

its Y-O-Y transactionmovement

increased by 6.7%.

Fromdata shared by iPropertyiq.

com, themost transacted areas in

Selangor were:

1) Klang

2) Shah Alam

3) Puchong

4) Ampang

5) Cheras

6) Kajang

7) Seri Kembangan

8) Petaling Jaya

9) Subang Jaya

10) Kapar

These top 10 areas comprise 50%of

(roughly 14,234) the number of

transactions of sub-sale residential

sales in Selangor (refer B).

Looking at the top transacted

areas, it was noted that transaction

volume fell across all areas except

for Setia Alamwhich rose by 15.4%

in sales, from 596 to 688

transactions. This is said to be

caused by the price factor.

In all, 11 other areas in Selangor

performed better than the state’s

average of -20.4%, with four doing

above average – Subang Jaya,

Cheras, Petaling Jaya and Shah

Alam.

Price wise, capital appreciation

for each state is measured by the

annual change inmedian prices per

sf. Fromdata recorded, all states

flourished except for Sabah.

Selangor fared below average

while Johor led the pack, more than

doubling that of Selangor’s

performance, four times more than

KL’s performance. Johor’s median

price per sf increased to RM266 psf

fromRM221 psf.

In terms of Y-O-Y capital growth

performance in Selangor, Puncak

Alamemerged tops with annual

capital growth reaching 23.4% (refer

A). Performing above average were

Kapar, Seri Kembangan and Klang.

Of the top 10 areas, Subang Jaya and

Petaling Jaya suffered capital

depreciationwith values declining

by 0.14% and 1.7% respectively.

Residential prices in Setia Alam

dropped in value by 8.5%, from

RM397 psf to RM368 psf.

While terrace homes measuring

1,500sf to 2,000sf made the cut as the

most popular product type aspiring

home buyers searched for, themost

popular products that were actually

sold turned out to be flatsmeasuring

500sf to 700sf, costing below

RM100,000 (refer D). Information

garnered fromdata revealed that

that there is a huge difference

betweenwhat home buyers are

interested in andwhat they are

purchasing. Affordability could be

themain reason.

In all, there are plusses and

minusses, whether buying newor

sub-sale. Weigh the pros and cons

and do your research beforemaking

a decision. While newproperties

may cost more (depending on the

size, location, etc.), sub-sale

residentials can come with a can of

worms or bring you years of happy

and comfortable living.

Followour column next week on

interior decor, followed by

residential sub-salemarket reports

on Johor and Penang.

>Graphs, charts and information on the Selangor market

Worth considering

SELANGORCAPITAL GROWTH YEAR-ON-YEARCHANGE (%)

+23%(RM257psf)

Capital Growth YoY Change (%)

20

15

10

5

0

-5

OverallSelangorY-O-Ychange (+7.4%)

-8.5%

(RM368psf)

PUNCAKALAM

SUNWAY

BANDARKINRARA

KAPAR

ULUKELANG

TANJONGDUABELAS

SUNGAIBULOH

SERIKEMBANGAN

KLANG

KOTADAMANSARA

SEPANG

SELAYANG

RAWANG

SEMENYIH

AMPANG

KAJANG

BATUCAVES

SERENDAH

PUCHONG

DAMANSARAPERDANA

BANGI

SHAHALAM

KEPONG

DAMASARADAMAI

CHERAS

PETALINGJAYA

SUBANGJAYA

SETIAALAM

Top10 transactedareas inSelangor

PUNCAKALAM

SUNWAY

BANDARKINRARA

KAPAR

ULUKELANG

TANJONGDUABELAS

SUNGAIBULOH

SERIKEMBANGAN

KLANG

KOTADAMANSARA

SEPANG

SELAYANG

RAWANG

SEMENYIH

AMPANG

KAJANG

BATUCAVES

SERENDAH

PUCHONG

DAMANSARAPERDANA

BANGI

SHAHALAM

KEPONG

DAMASARADAMAI

CHERAS

PETALINGJAYA

SUBANGJAYA

SETIAALAM

YoY Transaction Change (%)

15

10

5

0

-5

-10

-15

-20

-25

-30

-35

15.4%

OverallSelangorY-O-Ychange(-20.4%)

35.4%

SELANGOR TRANSACTIONS Y-O-Y CHANGE (%)

TRANSACTION VOLUME BY STATE (%)

Selangor

Johor

KualaLumpur

Penang

Perak

Kedah

N.Sembilan

Sarawak

Pahang

Malacca

Terengganu

Sabah

Kelantan

Perlis

Labuan

Putrajaya

TransactionsMarketShare (%)

30

25

20

15

10

5

0

31.7

14

9

8.2

7.9

6.1

5.4

4.3

3.5

3.4

2.6

2.3

1.1

0.2

0.2

0.1

SOLD – MOST POPULAR PRODUCTS SOLD

COMPARED TO LEADS RECEIVED

Sold

Leads

Terrace

500-750sf

RM192k

Terrace

750-1,000sf

RM278k

Terrace

1,500-2,000sf

RM625k

Apartment

750-1,000sf

RM255k

Flat

500-700sf

RM100k

Setia Alam, which recorded 688 sales compared to 596

previously, is the only area in Selangor which did not experience

a drop in transactions. Is price the factor?

Setia Alam experienced the biggest

drop in value in Selangor.

PJ (0.1%) and Subang Jaya (2%) is the only other two areas in

Selangor that have experienced a value drop as well.

28,467

sold

(-20.4%y-o-y)

Malaysia

Transaction

Volume

RM89.8k

(-17.6%y-o-y)

Residential sub-sale market report

A

B

C

D

20

theSun ON FRIDAY

|

MARCH11,2016

22

theSun ON FRIDAY

|

JULY28,2017