6 / 7

6 / 7

eligibility proposed by the

government, may stimulate some

residential sales, apart fromother

plans to increase the number of

units of low andmediumcost,

the largemarket supply remains

unabated, loan growth is expected

to slow further as the weak credit

cycle continues.

Apart from the stringent loan

requirements from financial

institutions that are said to have

caused the drop in the number of

property transactions, the

increasing cost of living and

economic uncertainties have led to

an upswing inworries about job

security, resulting inmore cautious

consumer spending. These and

more will have led themarket to

H

AVING

over the past two

weeks written on the global

and regional real estate

outlook, this weekwe

feature CBRE /WTW’s overviewof

2016 andwhat can be expected in

2017.

2016 OVERVIEW

Fundamentally, you could say that

the property industry runs

alongside the economy of the

country. As reported in CBRE /

WTW’s report, domestic

consumption rose, driven by

spending in areas that include F&B,

transportation and communication.

Government consumption also

grew (according to year-on-year

basis) – with expenditure owing to

infrastructure.

Net exports sawmixed results –

slower demand fromChina and

reduced exports from the US but

the weakening ringgit enticing and

increasingMalaysian exports even

further. The weak ringgit also

opened opportunities for foreign

investment.

Other than the global rout in oil

prices that has led to a significant

number of layoffs in the oil and gas

sector, the weakening business

sentiment and slowdown in the

overall trading is also expected to be

more apparent, but in the short

term.

Looking positive was the growth

rate of retail sales which

remained buoyant despite

softer consumer spending and

the rising costs of living.

According to the report,

strong support was seen from

tourists in retail spending

from shopping. The

weakening ringgit is expected

to encourage tourists’

spending.

2017 OUTLOOK

In the Year of the Rooster, the

country’s economic growth is

expected to be slower due to

PHOTO: HTTP://WWW.PROPERTYGURU.COM.MY

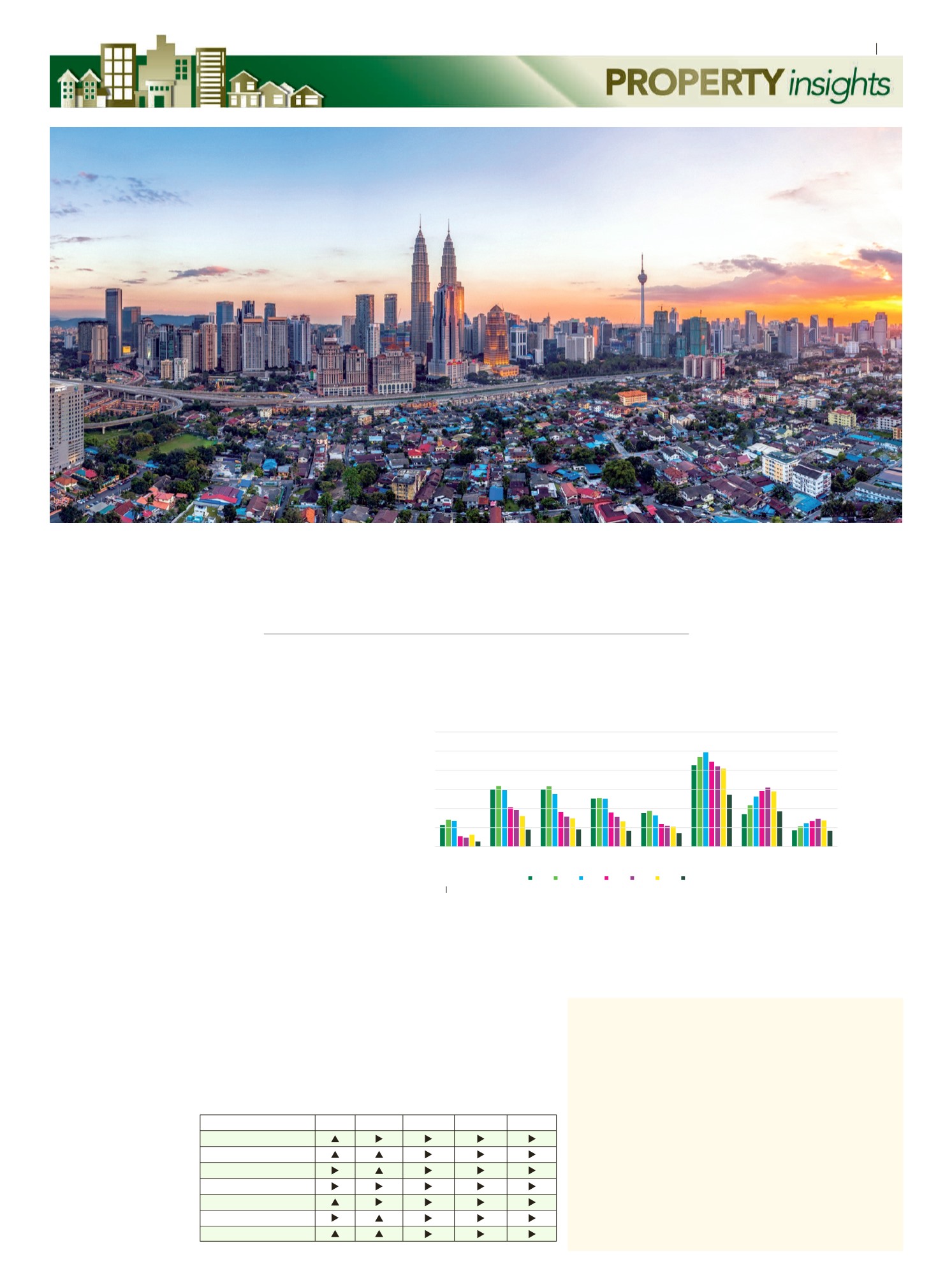

Malaysia real estate

market outlook for 2017

>CBRE /WTWreport on 2016 overviewand 2017 forecasts

the challenging global economic

and financial landscape. Domestic

demand is said to be the key driver

of growth, sustained primarily by

economic activity from the private

sector. Due to the well diversified

nature of our country’s exports,

positive growth is projected into the

year. However, inflation is expected

to remain flat although pressured by

increase of several price-

administered items and the weak

ringgit exchange rate.

The impact of these cost factors

on inflation is expected to be

mitigated by continued low global

energy prices, generally subdued

global inflation andmoremoderate

domestic demand. Supportive fiscal

andmonetary policies are also

expected to help steady the ship for

economic growth. GSTwill

strengthen the government’s

revenue source to accommodate its

fiscal measures.

With the overall weakening

ringgit, low crude oil prices coupled

withworldwide geo-political issues

will continue to plague the economy

in 2017. No doubt, the year will be a

challenging one, but Malaysia’s

economy is anticipated to remain

stable with GDP growth estimated

at 4.2%.

REAL ESTATEMARKET

OUTLOOK INMALAYSIA

As uncertainties and concerns over

Transaction Volume

30000

Total Volume

25000

20000

15000

10000

5000

50,000 & Below

urce: NAPIC, CBRE WTW Research

50

,001 - 100,000 100

,001 -

150,000

2010 2011 2012 2013 2014 2015 9M2016

150,001 -

200,000

200,001 -

250,000

250,001 -

500,000

500,001 -

1,000,000

1,000,001 &

Above

0

INCREASING SHARE OF UNITS ABOVE RM500K, HOWEVER,

UNITS WITHIN RM250K-RM500K PRICE RANGE REMAIN HIGH

IN DEMAND

Landed Residential

High-Rise Residential

Purpose built Office

Retail

Hotel

Industrial

2012 2013

2014

2015

2016

Overview

UNCERTAINTIES AND CONCERNS OVER LARGE MARKET

SUPPLY REMAINS UNABATED

BOON

Property investment will remain one of the safest forms of

investment.

The demand for affordable housing is likely to become acute.

Genuine demandwill lead themarket.

Themarket is expected to cool downwith prices becomingmore

negotiable.

Areas with good transportation connectivity (nearMRT I & II,

HSR, highways) will continue to be hotspots.

Demographic forces will continue to drive underlying demand

for residential properties.

BANE

On-going concerns on the overall weak ringgit, low crude oil

prices andworldwide geo-political issues will continue to plague

the economy.

Challenging year for developers.

More savvy home buyers.

X

X

X

X

X

X

X

X

X

CONTINUEDON

NEXT PAGE

X

consist of more genuine purchasers

with speculative sentiments not as

strong as during the boomperiod.

As such, supply has remained

resilient with greater activity in

larger cities. The proposal to boost

public servants’ housing loan

21

theSun ON FRIDAY

|

JANUARY 27, 2017